Результаты для "ar1 model"

Авторегрессионная модель - Википедия

https://ru.wikipedia.org/wiki/%D0%90%D0%B2%D1%8...

Авторегрессионная (AR-) модель (англ. autoregressive model) — модель временных рядов, в которой значения временного ряда в данный момент линейно зависят от ...

autoregressive linear models ar(1) models - Stat@Duke

https://www2.stat.duke.edu/courses/Spring00/sta...

AUTOREGRESSIVE LINEAR MODELS. AR(1) MODELS. The zero-mean AR(1) model xt = xt 1 + t is a linear regression of the current value of the time series on the ...

Autoregressive model - Wikipedia

https://en.wikipedia.org/wiki/Autoregressive_model

In statistics, econometrics, and signal processing, an autoregressive (AR) model is a representation of a type of random process; as such, it can be used to ...

2.1 Autoregressive Models | Stan User's Guide

https://mc-stan.org/docs/2_21/stan-users-guide/...

Unlike the autoregressive model AR(1), which modeled the mean of the series as varying over time but left the noise term fixed, the ARCH(1) model takes the ...

AR1 Model fixes — Загрузки - HALF-LIFE Project Beta

https://hl2-beta.ru/index.php?action=downloads;...

3 дек. 2017 г. ... AR1 Model fixes — Загрузки — HALF-LIFE Project Beta.

Autoregressive (AR) Model for Time Series Forecasting

https://www.geeksforgeeks.org/data-analysis/aut...

23 июл. 2025 г. ... Autoregressive models (AR models) are a concept in time series analysis and forecasting that captures the relationship between an observation and several ...

A unified view of linear AR(1) models - Rob Hyndman

https://robjhyndman.com/papers/ar1.pdf

Many models have been proposed as non-Gaussian analogues of the Gaussian AR(1) model (more than 30 such models are reviewed or discussed in this paper). We ...

22. AR1 Processes - Quantitative Economics with Julia

https://julia.quantecon.org/introduction_dynami...

In this lecture we are going to study a very simple class of stochastic models called AR(1) processes. These simple models are used again and again in economic ...

A Simple Example: Multilevel Manifest AR(1) Model

https://cran.r-project.org/web/packages/mlts/vi...

25 апр. 2024 г. ... A Simple Example: Multilevel Manifest AR(1) Model · #> Call: · #> mlts_model(q = 1, max_lag = 1) · #> Time series variables as indicated by ...

Analysing unemployment data with the AR1 Model

https://haakonbakkagit.github.io/btopic115.html

22 мая 2019 г. ... In this topic, we would like to show what the AR(1) model is and how to use INLA to analyse practical data with AR(1) model.

🖼️ Изображения

OLS Estimation of the AR(1) Model - YouTube

www.youtube.com

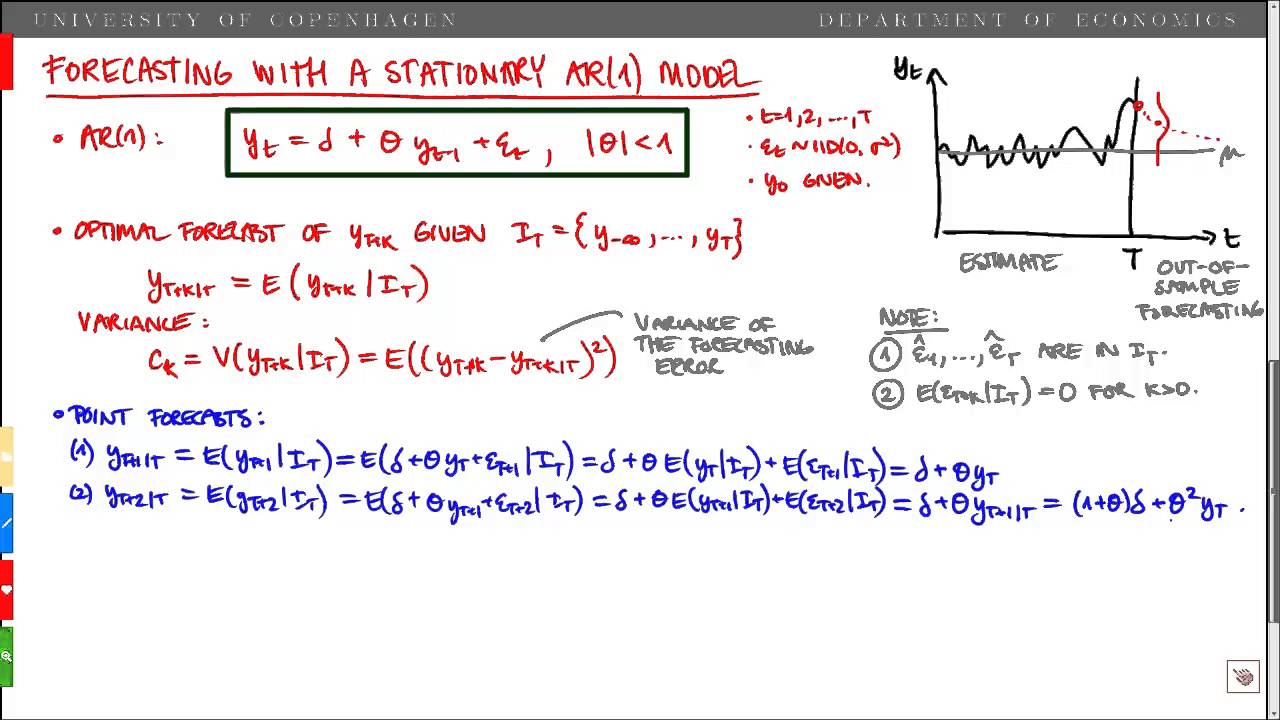

Forecasting With a Stationary AR(1) Model - YouTube

www.youtube.com

PPT - Environmentally Conscious Design & Manufacturing PowerPoint ...

www.slideserve.com

Autoregressive Model

gregorygundersen.com

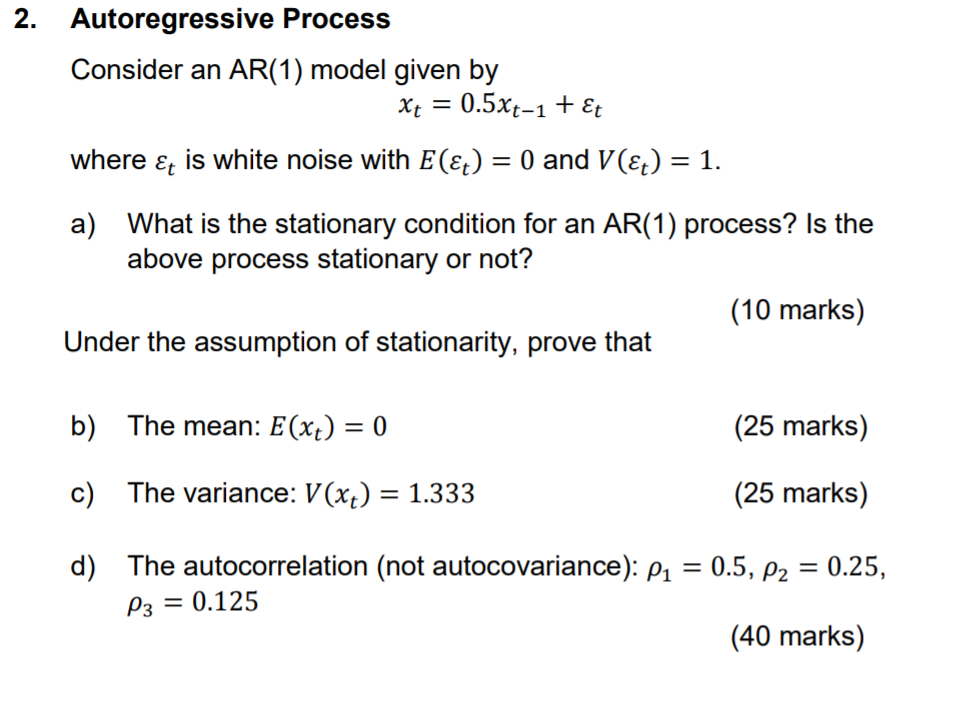

Solved 2. Autoregressive Process Consider an AR(1) model | Chegg.com

www.chegg.com

8.3 Autoregressive models | Forecasting: Principles and Practice (2nd ed)

otexts.com

Modelo AR(1) | Economipedia

economipedia.com

What are Autoregressive (AR) Models - YouTube

www.youtube.com

Autoregressive Processes are Gaussian Processes | Herb Susmann

herbsusmann.com

🎥 Видео

Modelling market risk: The AR1 model

YouTube • January 19, 2021 • 23:26

In this video we go through how to estimate AR(1)-models of market risk in the context of building a decision-support tool for risk management. The AR(1) model scores well on forecasting ability yet is simple and intuitive to use.

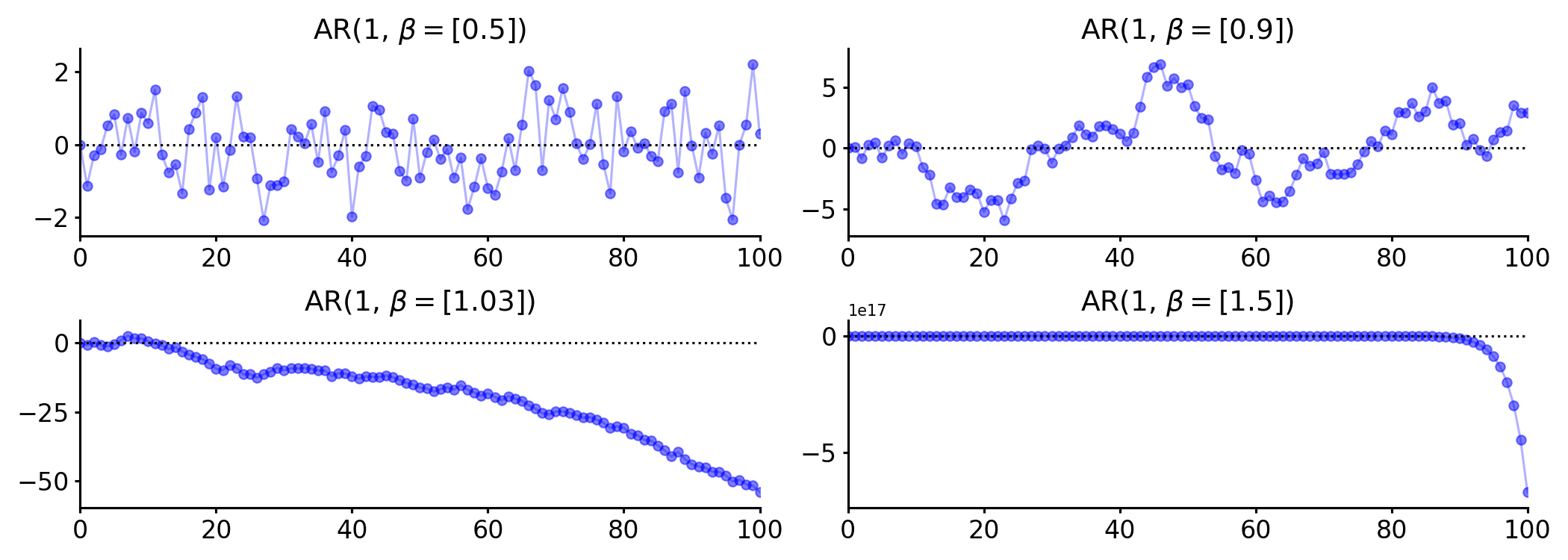

The AR(1) Model - Stationarity Condition and Properties Given Stationarity

YouTube • October 21, 2015 • 09:35

We present the stationarity condition for the AR(1) model and derive the properties of the model given stationarity.

OLS Estimation of the AR(1) Model

YouTube • February 20, 2017 • 07:44

We consider OLS estimation of the autoregressive parameter in the AR(1) model. Whenever the autoregressive paramter has true value between minus one and plus one, the OLS estimator is consistent.

Forecasting With a Stationary AR(1) Model

YouTube • October 27, 2015 • 09:18

We consider forecasting with a stationary AR(1) model. We derive the point forecasts and the variance of the forecasts one, two, and k periods ahead, and we show that these converge to the unconditional mean and variance, respectively, as the forecasting horizon goes to infinity.

Maximum Likelihood Estimation of the AR(1) Model

YouTube • February 20, 2017 • 10:10

We derive the likelihood function for the AR(1) model.

AR(1) Process: Mean, Variance, Autocovariance and Autocorrelation function.

YouTube • October 12, 2016 • 09:48

Full derivation of Mean, Variance, Autocovariance and Autocorrelation function of an Autoregressive Process of order 1 (AR(1)). We firstly derive the MA infinity respresentation of a stationary AR(1). Usng this we can then derive the relevant properties.